cz

cz

Tractors above 50 HP: lowest level in the past decade

When analysing the tractor market, we distinguish between two basic categories – machines up to 50 HP and above 50 HP. This is not merely a power classification, but two different market segments with a different customer structure. Tractors up to 50 HP are aimed primarily at smaller farms, municipal services or hobby users, while tractors above 50 HP fall into the category of machines used for agricultural operations.

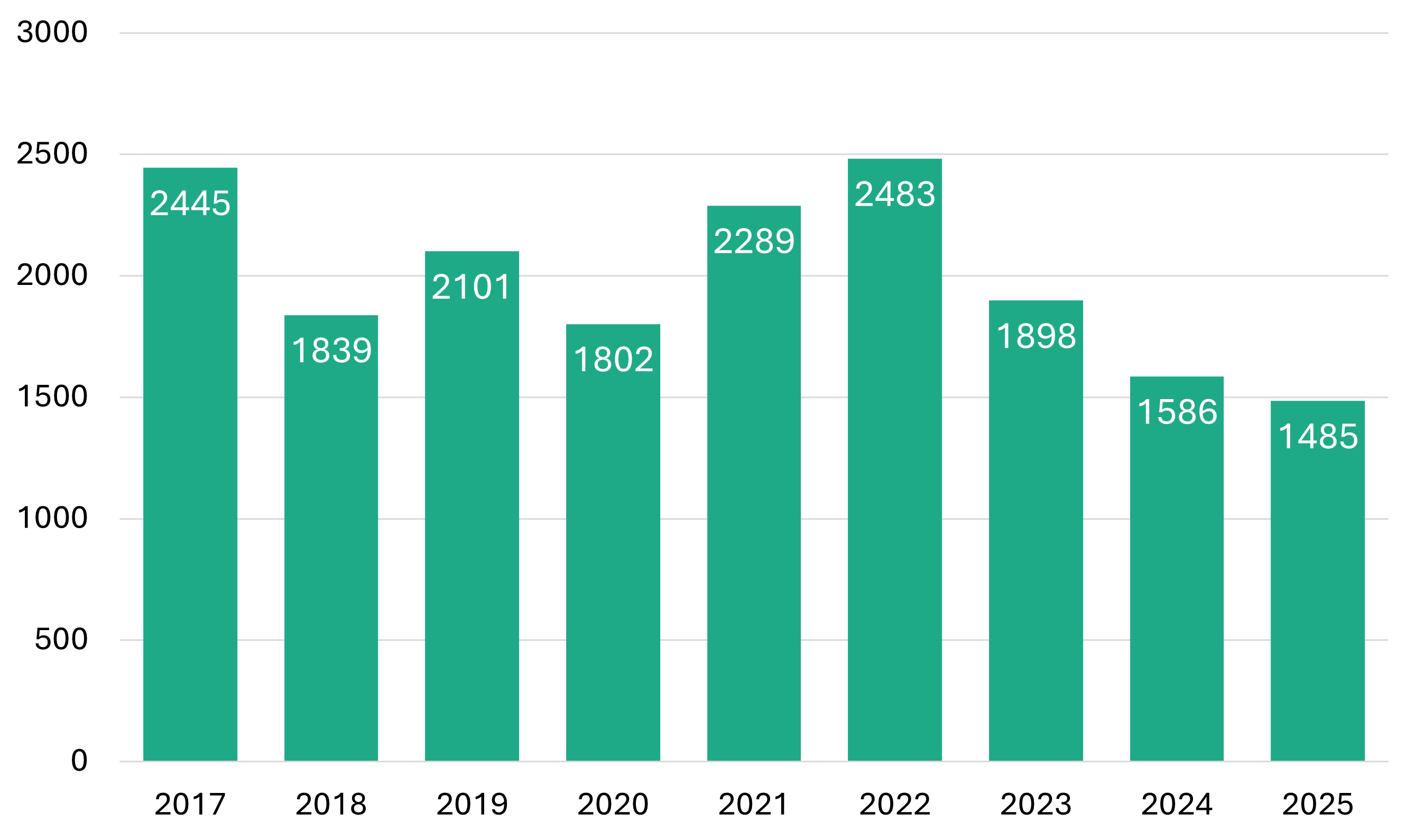

In 2025, a total of 2,332 new tractors were registered in the Czech Republic. In the category above 50 HP, this amounted to 1,485 machines, representing a year-on-year decline of 6% and at the same time the lowest result since 2017, when the Association of Agricultural Machinery Importers began systematically evaluating these data.

Registrations of tractors above 50 HP in 2017–2025 (units):

A more detailed look at the structure of power categories shows an interesting shift in the trend. While in previous years sales of tractors above 250 HP weakened the most, in 2025 this was the only segment to grow (+12%). The largest decline, by contrast, was recorded by tractors in the 50–150 HP range, i.e. machines used mainly by medium-sized farms.

John Deere remains the market leader with 301 registered tractors and a market share of 20.3%. Case IH and New Holland took second and third place. If the CNH Group is considered as a whole (New Holland, Case IH and Steyr), its combined share reaches 24%.

Fendt ranked fourth. Although it did not defend its second place from 2024, the brand has been successfully increasing its market share over the long term. Massey Ferguson and Deutz-Fahr managed to increase the number of registrations even in a declining market and achieved their highest market share in the past five years.

Registrations of tractors above 50 HP in 2025 by brand:

| Brand | Units | Market share |

|---|---|---|

| JOHN DEERE | 301 | 20.3% |

| CASE IH | 156 | 10.5% |

| NEW HOLLAND | 154 | 10.4% |

| FENDT | 137 | 9.2% |

| MASSEY Ferguson | 116 | 7.8% |

| DEUTZ-FAHR | 114 | 7.7% |

| CLAAS | 81 | 5.5% |

| VALTRA | 73 | 4.9% |

| KUBOTA | 69 | 4.6% |

| KIOTI | 57 | 3.8% |

| STEYR | 46 | 3.1% |

| Others | 181 | 12.2% |

| Total | 1 485 | 100% |

Segment up to 50 HP: dominance of Asian brands

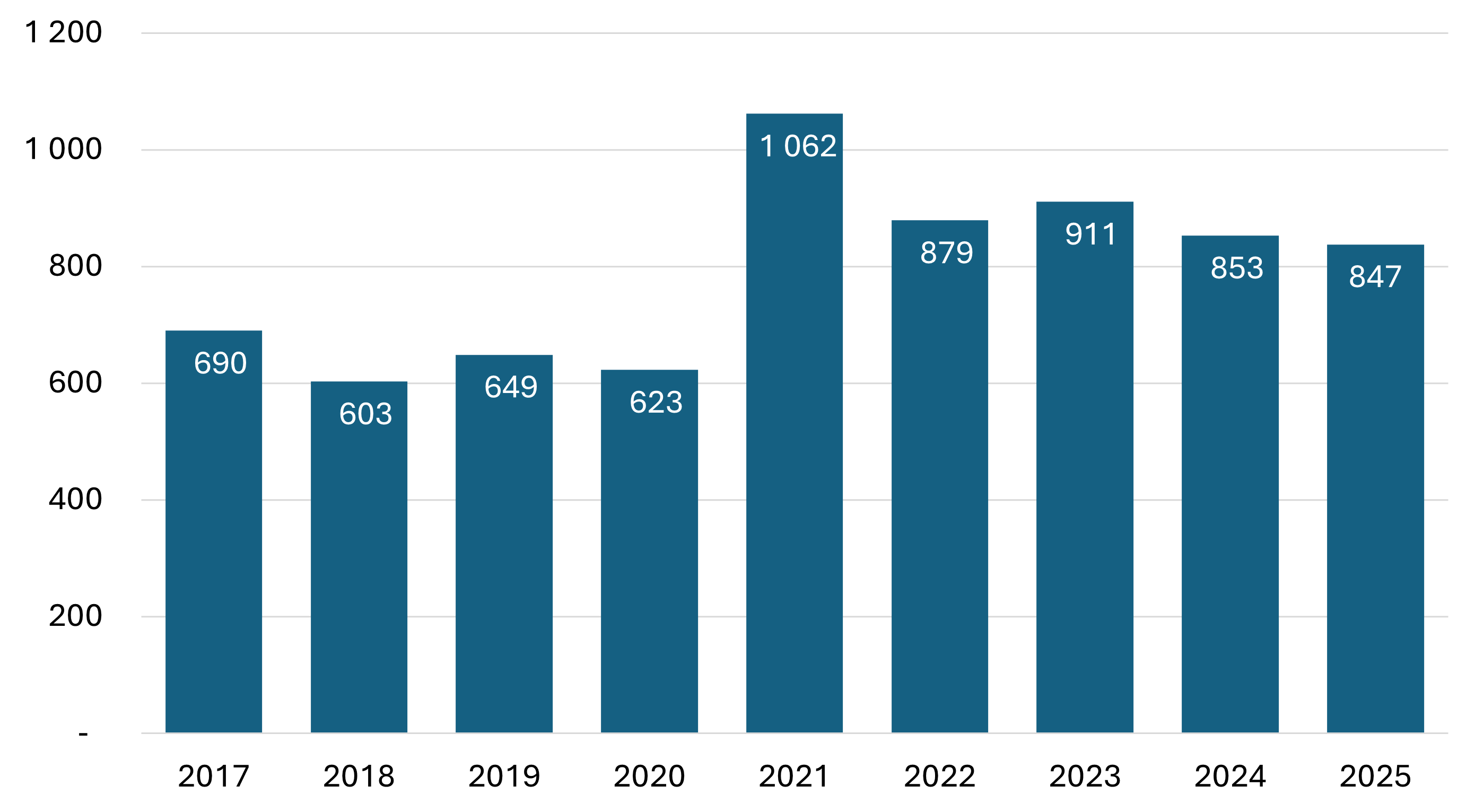

In the category of tractors up to 50 HP, 847 machines were registered in 2025. The segment therefore declined by only 1% year-on-year and remained relatively stable. Compared with other categories, this market is less dependent on the economic situation in agriculture.

Solis remains the leader in this segment with a share of 25.9%, although its market share has been declining slightly for the third consecutive year. Kubota and Captain also weakened. By contrast, manufacturers such as Yanmar and LS Tractor are strengthening their positions, and new market players are gradually gaining ground.

Registrations of tractors up to 50 HP in 2017–2025 (units):

Registrations of tractors below 50 HP in 2025 by brand:

| Brand | Units | Market share |

|---|---|---|

| SOLIS | 219 | 25.9% |

| KUBOTA | 85 | 10.0% |

| CAPTAIN | 74 | 8.7% |

| KIOTI | 54 | 6.4% |

| ŠÁLEK | 50 | 5.9% |

| TYM | 44 | 5.2% |

| JOHN DEERE | 39 | 4.6% |

| PREET | 27 | 3.2% |

| FARMTRAC | 26 | 3.1% |

| YANMAR | 24 | 2.8% |

| LS MTRON | 22 | 2.6% |

| ZYZKION | 22 | 2.6% |

| TAFE | 17 | 2.0% |

| TAUROS | 17 | 2.0% |

| Others | 127 | 15.0% |

| Total | 847 | 100% |

Combine harvesters: market fell by almost half

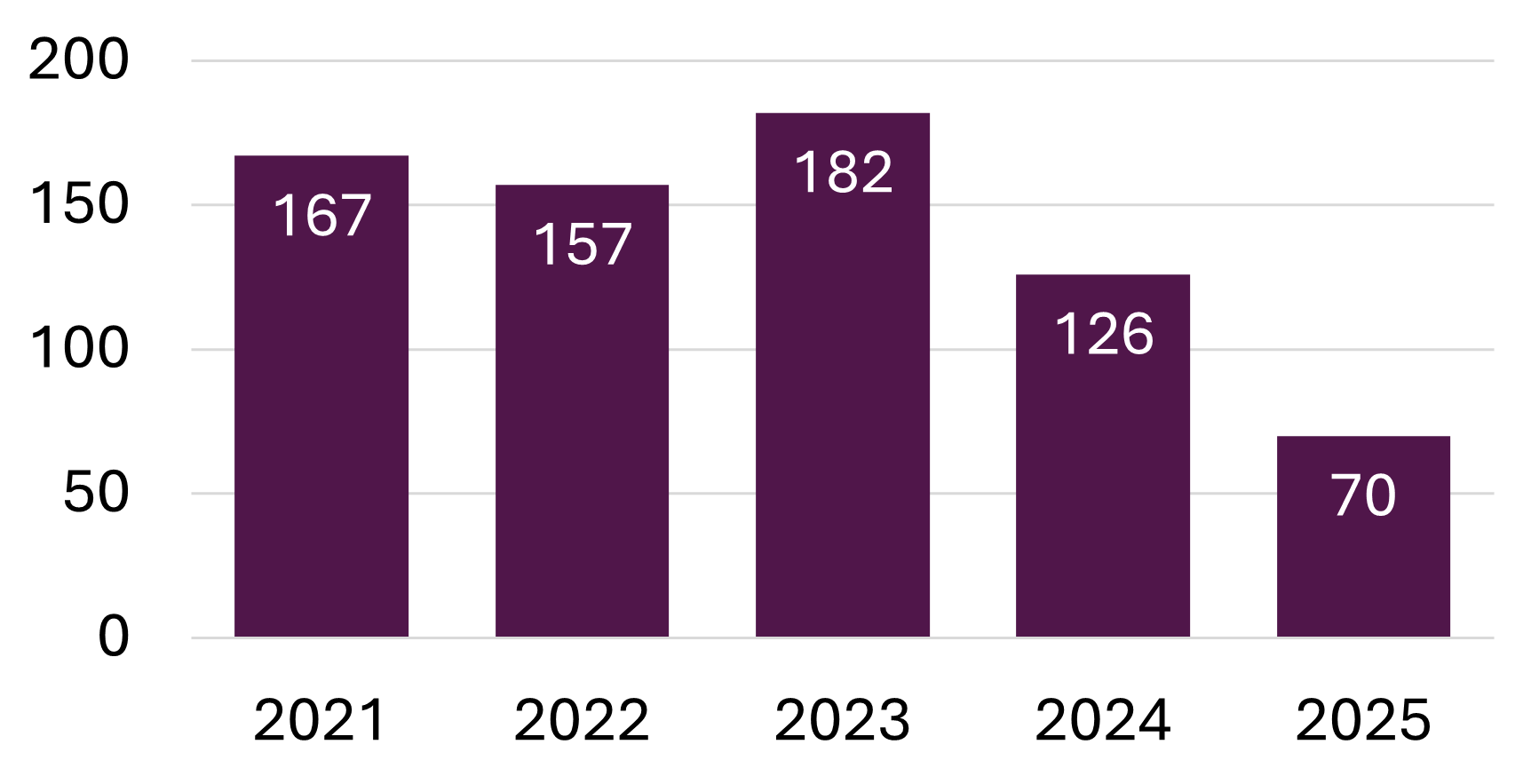

The year 2025 was exceptionally weak for the combine harvester segment. A total of 70 new machines were registered, representing a year-on-year decline of 44%. Compared with 2023, when 182 combines were registered, the market has fallen to less than half within two years.

The highest number of registrations was recorded by Claas and New Holland (19 machines each). John Deere ranked third with 16 machines. Massey Ferguson and Sampo also had a relatively good year, improving their position in a significantly smaller market.

Registrations of combine harvesters in 2025 by brand:

| Brand | Units | Market share |

|---|---|---|

| CLAAS | 19 | 27% |

| NEW HOLLAND | 19 | 27% |

| JOHN DEERE | 16 | 23% |

| CASE IH | 4 | 6% |

| MASSEY FERGUSON | 6 | 9% |

| FENDT | 3 | 4% |

| SAMPO | 3 | 4% |

| Total | 70 | 100% |

Forage harvesters: modest recovery

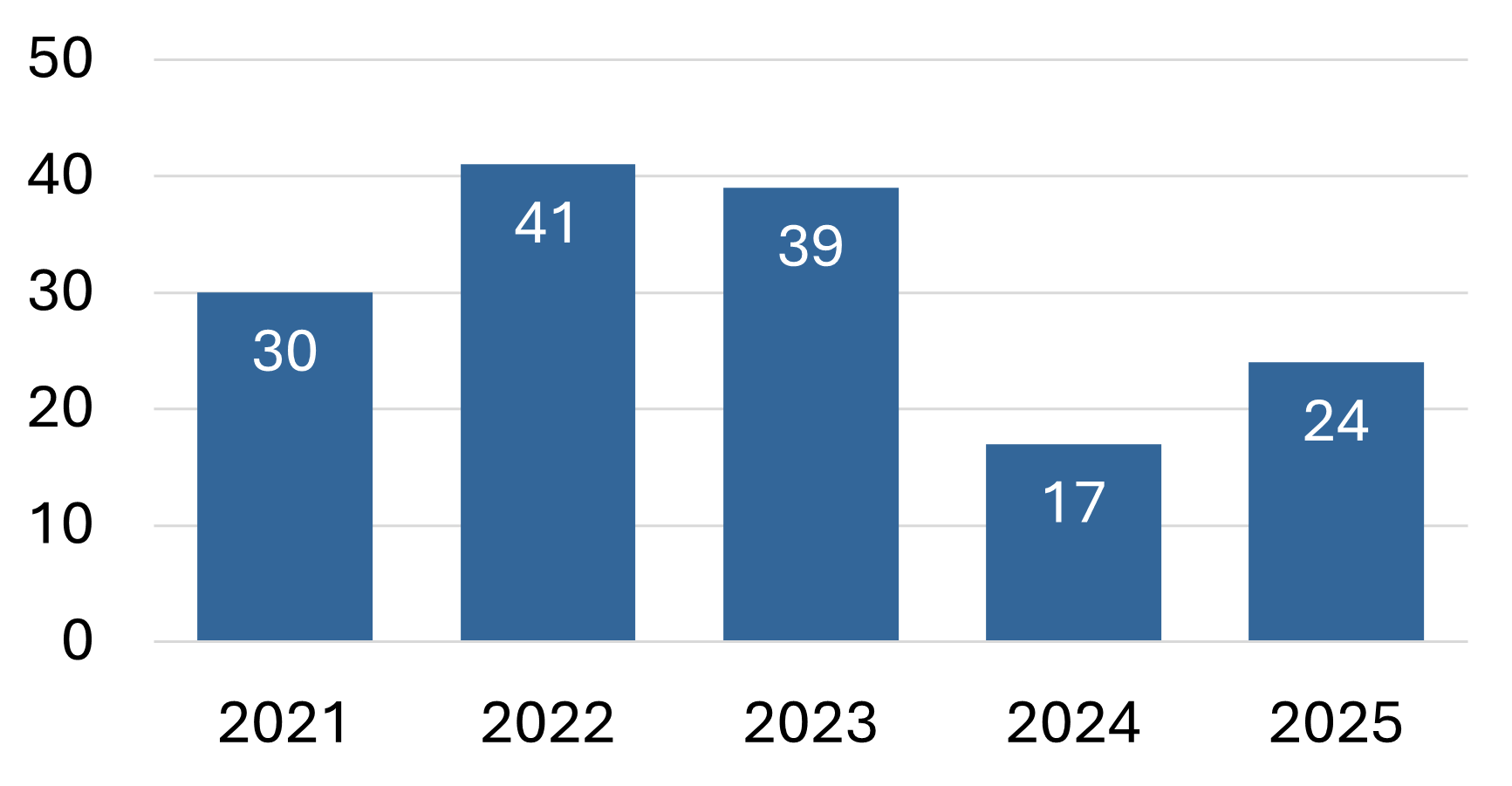

Unlike combine harvesters, the forage harvester segment recorded year-on-year growth. A total of 24 machines were registered, seven more than in 2024.

Claas strengthened its dominant position with a 42% share. It was followed by Krone, John Deere and New Holland. Despite the year-on-year growth, however, this segment remains below its long-term average.

Registrations of forage harvesters in 2025 by brand:

| Brand | Units | Market share |

|---|---|---|

| CLAAS | 10 | 42% |

| KRONE | 6 | 25% |

| JOHN DEERE | 5 | 21% |

| NEW HOLLAND | 3 | 13% |

| Total | 24 | 100% |

Most of Europe in the red

Compared with other European markets, the development of the Czech market in 2025 is not exceptional. Significant declines were recorded, for example, in Germany (-12%), France (-20%), Denmark (-27%), the Netherlands (-11%) and the United Kingdom (-14%). More moderate decreases were recorded in Austria, Sweden and Belgium.

Growth was rather the exception – Poland (+23.5%), Italy (+14.1%) and Slovakia (+35%) strengthened significantly. According to data from the Agrion association, Slovakia recorded its highest registrations last year since 2013, when Agrion began monitoring these statistics. While 669 tractors above 50 HP were registered in Slovakia in 2024, the market grew to 904 machines in 2025. The best-selling brand in the category above 50 HP was John Deere (182 units; 20.1%), followed by New Holland (152 units; 16.8%) and Case IH (93 units; 10.3%).

Expectations for 2026

In terms of sales volume, 2025 can be described as one of the weakest years of the past decade. Further market development will be influenced primarily by agricultural commodity prices, geopolitical developments in Europe and worldwide, and possible turbulence in global markets, which may affect the economic situation of agricultural enterprises. An internal survey conducted by the Association of Agricultural Machinery Importers among its members indicates a rather cautious outlook for the first half of 2026. Only 24% of respondents expect market growth, while 32% anticipate a further decline. The largest share of companies (44%) expect stagnation.

Martin Jurkovič